Bonds — they hold ions and people together, and as it turns out, can also serve as a form of investment. Bonds can strengthen an investment portfolio’s risk-return profile and provide diversification to navigate the waves of market volatility. Before we get into the specifics of it all, let’s first discuss what bonds are.

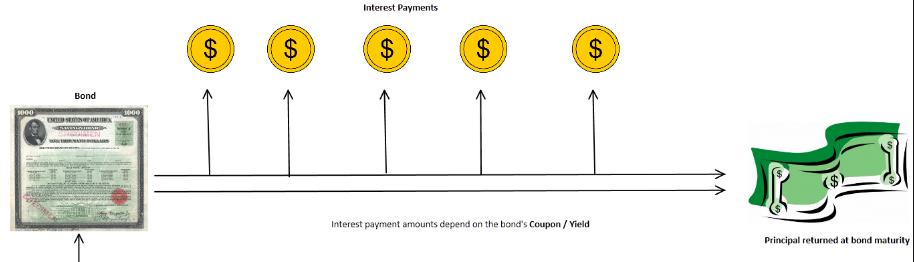

A bond is a certificate or loan taken out by a company or corporation that the borrower promises to repay within a certain time period. The difference between a bond and a regular loan is that instead of turning to the bank, the entity in need of the capital will get the money from investors who buy its bonds. In exchange for getting loaned the money, the borrower - which oftentimes can be a government entity, municipality, or company - will agree to pay a certain amount of interest per year. This is usually a percentage of the amount loaned and will be repaid at predetermined intervals until the end of the loan period.

It’s important to note that bondholders do not own any part of the companies they lend to, nor are they able to vote on company matters like stockholders do. Instead, bondholders are entitled to receive the amount that was agreed upon, as well as the principal of the bond. For investors looking to purchase bonds, there are a number of factors to consider when it comes to the bond’s price.

Bond Prices:

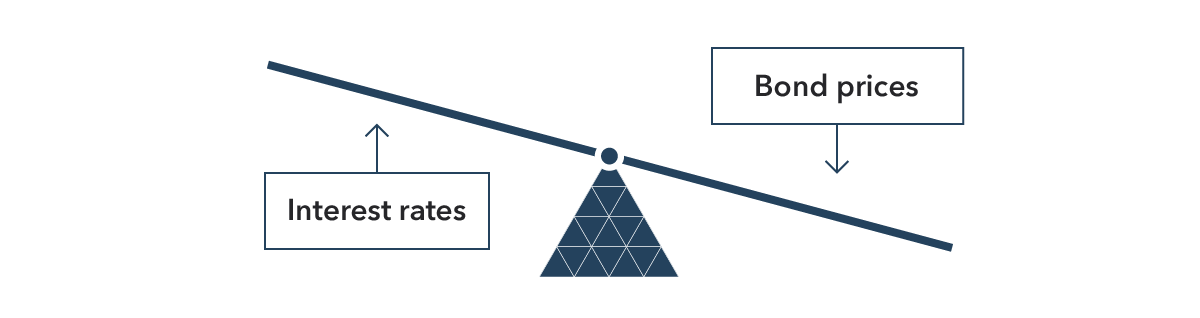

Bond prices can differ from their face values, or the price at which they are generally issued at, because the prices of the bonds are correlated to the current market rates. In addition, a bond yield is the annual return the investor can expect if the bond is held to maturity. The combination of the bond price and the bond yield at the original point of purchase is a huge determining factor for its price in the open market, or “secondary market.” Most bonds are traded over-the-counter between larger brokers and their clients. From here, however, bonds can also be sold in the secondary market once they’ve been issued.

Ultimately, the price of a bond can change according to the changes in the market. Therefore, if an investor were to sell a bond before it matures, the bond may be worth less than the value that was originally paid. Alternatively, if an issuer chooses to buy back a bond at the full face value before the maturity date, this is called a callable bond.

Why Invest in Bonds?

There are a number of reasons why investors choose to purchase bonds, including capital preservation, portfolio diversification, and protection against economic downturns or slowdowns.

- Investors who do not want to lose their capital or those who need to meet a liability at a specific time in the future may find bonds a great investment since they are meant to be repaid at a specific date, when the bond matures. Bonds can also sometimes offer higher interest rates than short-term savings rates, which provides investors with a greater incentive. Additionally, if an investor is able to sell a bond after its price has increased before maturity, they can appreciate the capital on their bonds and increase their total return, which is a combination of income and capital appreciation.

- For some bonds, the investor will receive a “fixed” income in which they receive interest payments on a set schedule, which can be used freely or to reinvest in other bonds.

- Another reason investors may purchase bonds is to diversify their portfolio. This is an important thing that many investors will do because it’s risky to “put all your eggs in one basket.” For example, if your portfolio is not diversified enough, your investments can end up taking a big hit if that industry sector is affected in the market. By adding bonds to the portfolio, investors can have a broad range of assets and equities that reduce the risk of negative or low returns on their investments.

- Bonds can also provide investors with protection against economic downturns, such as the one we are currently facing. As you know, economic downturns or slowdowns can often be unexpected and can put investors in a tough spot. The great thing about bonds is that they mostly pay a fixed income regardless of economic conditions. Especially in the case of a slowdown, bonds become more attractive to investors as they can purchase more goods and services with the same bond income.

Types of Bonds:

Now that we’ve discussed why investors may purchase bonds, there are many types of bonds to cover.

- Government bonds, which are issued and backed by central governments have historically been linked to inflation, which can experience greater losses than normal bonds in the face of fluctuating interest rates. Within government bonds, there are:

- Agency and quasi-government bonds, which support affordable housing developments or small businesses through agencies and

- Local government bonds, which are generally used to finance projects for communities or infrastructure such as building bridges, supporting schools, or other general functions.

- Corporate bonds are bonds that companies issue to fund their expansions or ventures.

- Emerging market bonds: Both government and corporate bonds that are issued by developing countries are known as emerging bonds. These types of bonds can help to diversify an investment portfolio and can provide risk-adjusted returns.

Most important aspects to consider when investing in bonds:

Investing in bonds is a big commitment, and investors should consider every aspect in full before making any purchases. Here are four important aspects investors should consider before purchasing a bond:

- Maturity: Bond maturity is the future date in which the principal of the bond must be paid to the investor and the bond’s obligations come to a close. Bonds typically come in three general types according to their lifetimes, including:

- Short-term: Mature within 1-3 years

- Medium-term: Mature in over 10 years

- Long-term: Mature in 10+ years

Bond prices are actually pretty heavily influenced by maturity. The rule of thumb usually is that the longer the maturity, the greater the change in price for a change in interest rates. Because of this, bond fund managers will attempt to change the fund’s average maturity to anticipate changes in interest rates.

- Quality and ratings: Bond quality is based on a company’s creditworthiness rating which are often determined by bond rating agencies, including S&P, Moody’s Investors Service, and others—these organizations specifically specialize in judging bond quality. Ratings can range from AAA, which represent the highest-grade issuers to D for issuers who are less trustworthy. In other words, the higher the rating, the lower the risk of the investment. It’s worthy to note that the only bond considered to be risk free is the U.S. Treasury Bond.

|

Highest Quality |

Moody's |

Standard & Poor's |

|

High Quality |

Aaa |

AAA |

|

Good Quality |

Aa |

AA |

|

Medium Quality |

Baa |

BBB |

|

Speculative Elements |

Ba |

BB |

|

Speculative |

B |

B |

|

More Speculative |

Caa |

CCC |

|

Highly Speculative |

Ca |

CC |

|

In Default |

- |

D |

|

Not Rated |

N |

N |

- Issuing organization: As we previously discussed, bonds can be issued by governments, municipalities, corporations, and brokers. The U.S. government can also issue securities, which are typically considered to have the most safety. When considering whether you should purchase bond funds directly or through a mutual fund, it’s important to understand that mutual funds hold multiple bonds and make it impossible to lock in the payment rate or principal. On the other hand, this is something you’d be able to control if directly buying the fund.

However, bond fund managers also have more resources that they can make the most of - more than an individual investor could. Make sure you do your research before deciding if you should buy bonds yourself or through a broker.

- Callability or call provisions: A "call" is when the issuer of the bonds has an opportunity to redeem the bonds after a certain specified amount of time has passed. In some cases, bonds can be paid off by the issuer before it reaches the point of maturity. These bonds typically offer better coupon rates.

However, just because these bonds can be paid off at an earlier date, this doesn't guarantee a continuation of a high yield after the call date. Instead, it can actually limit the appreciation of the bonds, and in turn, make the investment more risky. These call provisions can be complex, so it is best for investors that don't have strong knowledge to avoid bonds with a call feature.

- Liquidity: The ability to sell a bond after purchase has a major role in bond buying. If you purchase a bond and want to sell it, you’ll have to find a buyer. Similarly, investing in a bond fund means the fund has to buy your shares back at any time you wish.

There’s a lot to consider when it comes to investing in bonds, but it can be truly worth your time and investment if done right. If you’re still curious about the investment process and want to speak to a financial expert, reach out to our team of certified CPAs today!